An elderly British man asks a homeseller if he used the real estate firm Purplebricks to sell his home.

“They’re just online, aren’t they?” asks the seller.

“No, no, they’re proper estate agents,” insists the elderly man. “You just don’t pay commission.”

Looking dazed, the seller politely excuses himself. Then he screams into a cupboard.

He has experienced “commisery,” viewers learn. It’s “the misery you feel when you spent thousands on commission but got nothing more for your money.”

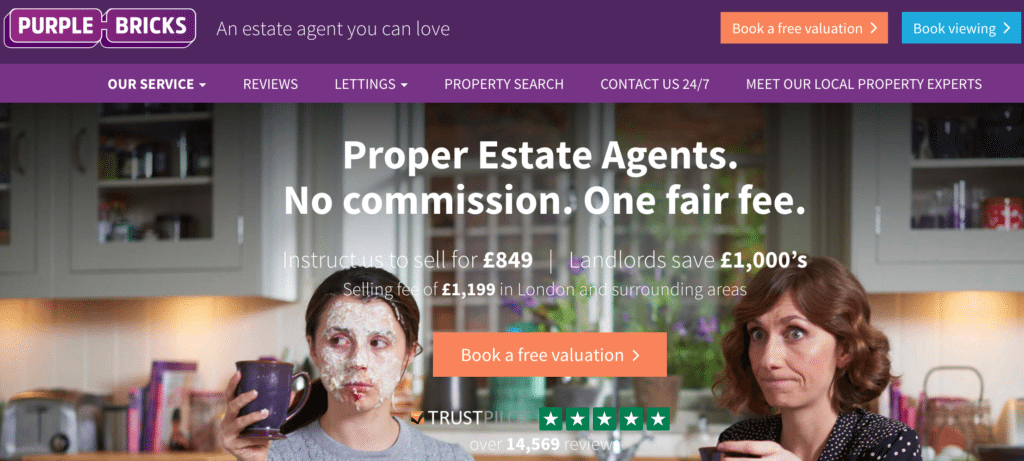

Ads like this have helped turn hybrid brokerage Purplebricks into one of the biggest real estate firms in the U.K. since launching three years ago.

Purplebricks offers a self-service technology platform and assistance from a local agent for a low fee. Agents provide pricing guidance, photographs and on-demand consulting. But sellers are encouraged to perform many tasks themselves, including negotiating offers.

Now the publicly traded company is gunning for the U.S., with plans to target a robust marketing campaign at Americans. In a special stock offering, the company recently raised 50 million pounds (around $62 million) to break into the U.S. in the second half of 2017.

Hoping to repeat its success in the U.K., Purplebricks will use a combination of high-volume agents, technology and low fees to try and gobble up market share.

But the upstart could face tough resistance from brokerages here, judging by the company’s experience in the U.K. And more importantly, it might struggle to win over consumers who have shrugged at low-fee offerings in the past.

Does this sound familiar?

This is not the first time a well-funded real estate startup thought it could take the U.S. by storm with a low fee.

Such firms have tended to change their business model or stall. (Take iPayOne or Your Home Direct, for example).

And it remains to be seen whether Purplebricks can adapt to a market with buyer’s agents, an unknown quantity in Britain.

In the U.K., Purplebricks charges around $1,000, compared to a typical commission of 1.5 percent. Commission rates are much lower in the U.K. than in the U.S., in part, because Brits don’t use buyer’s agents.

Customers must cough up the fee regardless of whether they sell their home, but they can delay payment for up to 10 months if they use Purplebricks’ recommended attorneys.

Since launching in 2014, Purplebricks has become the second biggest U.K. real estate brokerage, according to a spokesman. The spokesman said Purplebricks commands a U.K. market share ranging from 4 to 6 percent, though UBS estimates the number is actually 2.2 percent.

In September 2016, Purplebricks expanded to Australia, tweaking its service model to support property auctions, which are common there. It’s grown its Australian agent count to 50 so far.

The company, which is traded on the London Stock Exchange, boasted a market cap of around $930 million on March 16, according to Yahoo Finance. At the time, that was not much less than the combined value of three of its biggest U.K. competitors, Countrywide, Foxtons Group and LSL Property Services.

Since Purplebrick’s rise, Countrywide has launched an online service and admitted to lowering its fees due to pressure from digital competitors.

Purplebricks listing page

Dissenter voices

The U.K. industry has pushed back aggressively, accusing Purplebricks of providing poor service and claiming that the brokerage often sets up homesellers to fail.

Detractors cried foul when Purplebricks recently removed Facebook reviews from its Facebook page and replaced them with TrustPilot reviews.

Some speculate that Purplebricks uses manipulative tactics to inflate its TrustPilot reviews, such as by requesting reviews before customers have closed a sale. Purplebricks denies doing this.

One commenter on an article about Purplebricks expressed dismay as a “small independent” and described using “dummy” email accounts to request fake showings and property valuations to undercut online competitors and waste their time.

“Whilst these actions do take up time these companies are trying to destroy our businesses and our livelihoods — ‘disrupting’ them from getting market share is worth it in the long term,” the commenter said.

Purplebricks has claimed to convert about eight out of 10 listings into sales agreements and about nine out of 10 sales agreements into closings. An analyst who covers Purplebricks recently said the second figure was “significantly better” than his previous estimate.

Adapting to buyer’s agency

Existing criticisms may provide U.S. brokerages with ammunition. But adapting to the idiosyncrasies of the U.S. market will present the biggest challenge for the burgeoning U.K. firm.

Unlike in the U.K., U.S. real estate transactions generally depend on cooperation between buyer’s agents and listing agents, a system underpinned by the multiple listing service.

That means the company’s previous strategy of casting traditional agents as overpaid, while highly successful in the U.K., could backfire in the U.S., according to Michael DelPrete, an adviser to real estate tech startups. It might deter buyer’s agents from showing Purplebricks listings to prospective buyers, he said.

Purplebricks need look no further than its U.K. competitor Foxtons to appreciate the difficulty of blitzing into the U.S. with a low-fee offering. Foxtons acquired Your Home Direct — a high-tech, discount firm reviled by U.S. agents — for $20 million in 2001. The firm went under six years later.

U.S. hybrid brokerages such as Redfin have tended to gravitate toward a traditional business model, raising fees and providing more hands-on service over time.

The game plan

Purplebricks declined to discuss its U.S. expansion plans, citing a “blackout” period mandated under U.S. securities laws. But the company outlined its strategy in a U.K. regulatory filing.

Eric Eckardt — a founder of multiple real estate startups and the former vice president of online real estate at Altisource — will head up the expansion, leading an effort to hire “some of the most experienced real estate agents” to begin a rollout to key states in the second half of this year, the filing said.

Purplebricks will couple this recruiting push with a business model adapted to the U.S. market and a marketing campaign “built upon the company’s successful brand lead strategies in the U.K. and Australia,” according to the filing.

The firm’s U.S. digital platform will let buyers and sellers book a listing appointment, schedule showings, “approve listing particulars and advertisements,” receive showing feedback, “access information and advice, receive and negotiate offers and agree [to] a sale.”

Slide from Purplebricks’ latest earnings presentation. (“LPE,” short for local property expert, is Purplebricks’ term for its self-employed brokers.)

A focus on double-ending deals

Expanding from its roots as a listing broker, the company will also begin working with buyers for the first time, with an apparent focus on double-ending transactions.

One goal of Purplebricks’ marketing strategy will be to secure “buy side activity for Purplebricks properties,” the filing says.

By encouraging direct interaction between buyer and seller, Purplebricks’ platform could help the company double-end an unusually high share of deals.

Trelora, a low-fee brokerage that resembles Purplebricks, has used a direct messaging system for buyers and sellers to that end.

The business and licensing model

Echoing the value proposition of some other U.S. hybrid brokerages, Purplebricks said that the company’s platform and aggressive marketing “should allow agents to spend more time focusing on looking after customers and selling homes, rather than a significant proportion of their time being taken up prospecting for the next listing.”

Purplebricks will grant exclusive licenses to self-employed U.S. brokers to deploy the Purplebricks business model, technology and brand within specific ZIP codes.

In the U.K., such brokers share a cut of their revenue with Purplebricks, but they do not pay a licensing fee.

These brokers will run their own businesses with the option to hire agents. In the U.K., Purplebricks affiliates are required to hire additional agents once lead volume reaches a certain level.