- The prime rate moved mechanically to 3.50 percent, rising in lockstep as it will after each future increase in Fed funds.

- The stock market rose in relief that the Fed was not more aggressive in its words or projections, but has fainted since.

- Gold fell to a six-year low. Oil broke below $35 per barrel. Natural gas broke below two bucks.

We have liftoff. The long and short of it follow — short first.

The immediate reaction to the Fed’s first hike in 1- years, from a band “0 percent to .25 percent” to .50 percent: The prime rate moved mechanically to 3.50 percent, rising in lockstep as it will after each future increase in Fed funds.

Prime is the index for most home equity lines of credit, whose payments will rise in the next envelope, as will those for adjustable rate mortgages.

The stock market rose in relief that the Fed was not more aggressive in its words or projections, but has fainted since. Try not to pay attention to stocks, though. Once each year, maybe. Stocks are vulnerable to the Fed in part because the grand game of corporate borrowing to buy-back stocks is about to end.

Gold fell to a six-year low. Oil broke below $35 per barrel. Natural gas broke below two bucks. Charts appended are staggering.

Three mechanisms are in play in those markets:

- Demand is down, and appears more a structural decline than cyclical. China, the key player, is a mess, entering what anyone a year ago would call a “hard landing,” its reforms a bust.

- If the Fed intends a sustained march upward to fight inflation, then inflation assets aren’t worth buying.

- Since the Fed’s march will increase the value of the dollar (China and Argentina this week added to the competitive-devaluation spiral), then others would be wise to buy dollar-denominated assets: oil, natural gas, Treasurys….

Treasurys, oh, my. The definitive 10-year T-note has fallen in yield since the Fed’s move, slightly under the important 2.20 percent mark, while short term rates rose. 10s have traded down with the commodity complex and on weak stock days. More of that ahead, probably.

How far can the Fed push up the overnight cost of money before pushing up long-term rates, 10s and mortgages? In the near term, the harder the Fed pushes, the less inflation fear and the more overseas desire to buy dollar assets.

The Fed’s last tightening cycle is one guide to what’s ahead. The Fed cut the overnight rate fast in 2001, from 6.50 percent to 1.75 percent. Its prior tightening had more to do with bubble-busting than inflation, and its over-doing brought us to the edge of deflation.

Then from the cycle low at 1.00 percent in mid-2003, the Fed tightened to 5.25 percent in June 2006, when the great credit bubble began to blow. When the Fed began that tightening, the 10-year T-note was 3.20 percent and rose quickly to 4.8 percent but stayed below 5 percent throughout. Mortgages held between 5.50 percent and 6.50 percent.

Known at the time as “Greenspan’s Conundrum,” why would long-term rates stay the same while the Fed hiked the cost of money, ultimately above long-term rates?

Save that question. Bookmark it. One answer is the same as today: foreign money then wanted dollar assets. More important: short rates closing on long from underneath, and ultimately rising above…that’s the every-time signal that the Fed is creating a recession.

Central banks fight the thought. They think markets are behaving irrationally or special cases are in play, like foreign money. But today more than ever it’s one world out there.

The market is already shouting a warning to Yellen & Co. And they know. But they think they should be pre-emptive. Intercept future inflation risks, an overheated job market. All invisible, but the Fed has its duties, its forecasts calling for inflation to rise to or above its 2 percent target any year now, although its models have been mistaken for eight-straight years.

To get a perverse reaction at liftoff? Short rates up, long down? That’s the move typical of the end-stage, not the start. The historical record has no similar moment.

The outside world…This week we have new right-side governments in Venezuela and Argentina beginning financial repairs. Poland is tilting away from Euro-socialism. But the bad right is not gaining (Le Pen and such). Chairman Xi in oblivious comedy told a UN technology conference that each national government should control content in its Internet. The wave of the past, sir. Vladimir Putin yesterday said he likes Donald Trump best, and today The Donald blew a kiss back to him.

A light heart is a good thing at Christmas. MERRY to all!!

10-year T-note in the last week. Modestly frantic before the Fed meeting, down since.

10-year T-note in the last year. Exactly where it was one year ago.

Fed-predicting 2-year T-note in the last year. As in copy above, spread to 10s has narrowed from 1.80 percent to 1.15 percent.

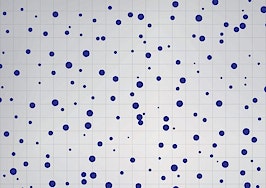

The Fed’s damned little dots, forecasting the Fed funds rate at the end of each year in the future. This scattergram has gradually come down in slope, in part because markets have told the Fed that it’s nuts. An important tipoff to Fed politics: the dots are from the five governors (appointed by the President and confirmned by the Senate) who run the place, and the 12 regional-Fed presidents, only five of whom vote at any given meeting. At least four of the regionals are rock-headed hawks — if you throw out the top four dots in the scattergram, you get a more reasonable forecast, only two or three hikes next year.

Gold since 1990. Believers have lost 40 percent in three years.

Oil in the last five years.

Natural gas in the last five years (off the back of the chart, ten years ago gas traded at $14):

Copper five years back. How’d you like to be a big producer of industrial metals?

Hard to read, but charts showing how very wrong about inflation the major central banks have been.

If inflation does begin to move up, as suggested in this chart, then long-term rates will rise — and a lot.

Lou Barnes is a mortgage broker based in Boulder, Colorado. He can be reached at lbarnes@pmglending.com.