Tight mortgage lending standards have dashed the hopes of many would-be homebuyers, but the developers of the most popular credit risk score today revealed some habits and behaviors of "high achievers" with FICO scores above 785.

More than 50 million people — about a quarter of all people with credit scores — are considered high achievers and tend to have "strikingly similar" credit habits regardless of background or life experience, San Jose, Calif.-based Fair Isaac Corp. said.

Some of these habits are fairly predictable: They keep low revolving balances relative to their available credit, don’t max out their credit cards, and consistently make payments on time.

But high achievers are not debt-free. They have an average of seven credit cards, including open and closed accounts, and carry balances on an average of four credit cards or loans. One-third have balances of more $8,500 on nonmortgage accounts.

Nevertheless, almost none — less than 1 percent — have an account past due. The overwhelming majority, 96 percent, have no missed payments on their credit report. Those who do have long since mended their ways — their last missed payment happened an average of four years ago.

The FICO score ranges from 300 to 850, and is used by virtually all lenders to gauge credit risk and the likelihood a borrower will repay a loan. The credit score can affect how much money a lender will offer and at what terms; higher credit scores mean borrowers can potentially save thousands of dollars over the life of a loan, FICO said.

Ellie Mae Inc., which provides mortgage origination software to lenders, reports that the average FICO score for mortgages approved in September was 750, with borrowers making down payments averaging 22 percent, having front-end debt-to-income ratios of 23 percent and back-end DTIs of 34 percent.

Those whose applications were denied had an average FICO score of 704, with borrowers willing to make down payments averaging 12 percent. The average front-end debt-to-income ratio was 27 percent; the average back-end DTI was 44 percent.

The average FICO scores for purchase mortgages eligible for purchase and guaranteed by Fannie Mae and Freddie Mac was 762 (compared with 729 for denied applications), while FICO scores on FHA-backed purchase loans averaged 701 (compared with 665 for denied applications).

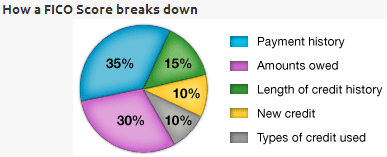

Because payment history makes up the biggest chunk of how a person’s FICO score is calculated — 35 percent — managing credit responsibly over time plays a large part towards improving one’s credit score, FICO said. This includes paying at least the minimum amount on all credit cards every month, the company added.

"Missing payments will lower a person’s FICO score, but if that happens, establishing or re-establishing a good track record of making payments on time will generally improve a person’s score," said Anthony Sprauve, credit score adviser for myFICO, the company’s consumer division, in a statement.

By law, most negative information, including missed payments, is removed from credit reports after seven years. This does not apply to tax liens or Chapter 7 bankruptcy. About 1 in 100 high achievers had a collection on their credit report, and about 1 in 9,000 had a tax lien or bankruptcy.

"While people with a high FICO score are not perfect, their consistently responsible financial behavior usually pays off over time," Sprauve said. "In a challenging economic period, the fact that we all have a chance to be high achievers is very good news. The lesson from these high achievers is that it’s never too late to rebuild and score high."

FICO high achievers typically have long, well-established credit histories and rarely open new accounts, FICO said. They opened their oldest credit account 25 years ago, on average, and their most recent credit account more than two years (28 months) ago. In general, their average credit account is 11 years old.

Their balances are often low and they use only an average of 7 percent of their available revolving credit, i.e., $70 on a credit card with a $1,000 maximum.

FICO considers both positive and negative credit report information within five general categories, the company said: payment history, amounts owed, length of credit history, new credit, and types of credit used.

Source: FICO

The FICO score does not take into account attributes such as race, gender, age, marital status, salary, employment history or address, the company said. FICO’s consumer website, myFICO.com, offers tips and tools to help people make decisions about their credit.

"Because a high FICO score is typically achieved over time and takes into account dozens of variables, there are no ‘quick fixes’ for rapidly improving scores or repairing bad credit," Sprauve said.

"Practicing good credit behavior consistently over time and regularly checking your credit report for errors can be instrumental for achieving a high credit score, which can lead to better loan terms and lower interest rates. Achieving good credit health is a long-distance event, not a sprint."